How your health insurance subsidies are calculated

In the 15 years since the Affordable Care Act was signed into law, subsidies have become a well-known part of health plans purchased on the Marketplace. The initial subsidies were further enhanced by the American Rescue Plan and the Inflation Reduction Act, ensuring that they remain a hallmark characteristic of the Affordable Care Act through 2025. For anyone who has looked into their options, your subsidy amount is shown even before you view the plans themselves. But how are the subsidy amounts actually determined?

This brief article explores how your income plays into your subsidy, how your Cost Sharing Reduction is calculated and your Premium Tax Credit, and what happens if your estimated income differs from your actual income at the end of the year.

There are two different types of subsidies that are available, the Premium Tax Credit and the Cost Share Reduction. Both subsidies are determined directly by how many people are in your household, how much money your household makes each year, and how many people are applying for coverage.

The Premium Tax Credit, or PTC, is available on every plan sold on the Marketplace and it’s purpose is to lower the amount you pay each month for your health coverage. The most common type of PTC is the Advanced Premium Tax Credit, or APTC. With the APTC, you estimate your income for the year to generate a subsidy amount. This amount is sent directly to the insurance company on your behalf.

Cost-Sharing Reductions, or CSR, are used to directly reduce your out-of-pocket cost by lowering the amount you are required to pay when you seek care. Plan deductibles, co-payments, coinsurance and the plan’s max-out-pocket amount are all reduced by a set percentage. The CSR is only available on Silver tier plans.

Eligibility

While most anyone can purchase a plan on the Marketplace, not everyone is eligible to receive a subsidy. The main stipulation is that you cannot have the option of receiving affordable healthcare elsewhere. For most people, this means that if your job (or your spouse’s job) offers you insurance, you cannot buy a Marketplace plan and receive a subsidy. There are a few stipulations with how much the group insurance cost and what it covers, so if you think you’re paying too much or not getting everything you need, it is worth talking to a broker to see what options you have.

Additionally, subsidies are only available to those who meet the criteria of having a projected income where the cost of the Benchmark Plan would exceed 8.5% of their estimated income. Finally, subsidies are not available to Catastrophic plan, which are generally only offered to individuals younger than 30.

What are Benchmark plans

Every year the base cost of all the Marketplace plans change. The new prices are set by the insurance companies based on the zip code where the plan is offered, but the government determines what features must be included in a plan, ensuring that what is offered is comparable. Because several companies offer what is essentially the same coverage, each company does it’s best to be competitive and offer plans at the lowest rate.

Once plan prices are set, the second lowest priced Silver plan is used as the Benchmark Plan for that year in that specific zip code. The premium of that Benchmark Plan is then used when determining the PTC and APTC subsidy amounts.

Premium Tax Credits

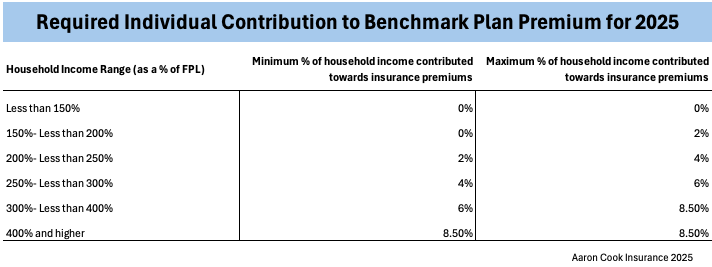

The PTC and APTC subsidies operate on a sliding scale that creates a direct and inverse correlation with income- the more money you bring in, the larger the share you are expected to pay, which in turn decreases your subsidy amount. Prior to the American Rescue Plan in 2021 & then the Inflation Reduction Act in 2022, there was something known as the ‘Subsidy Cliff.’ This loophole in the framework of the original ACA, along with the ‘Family Glitch,’ has been patched, capping the percentage of income paid towards insurance premiums at 8.5%.

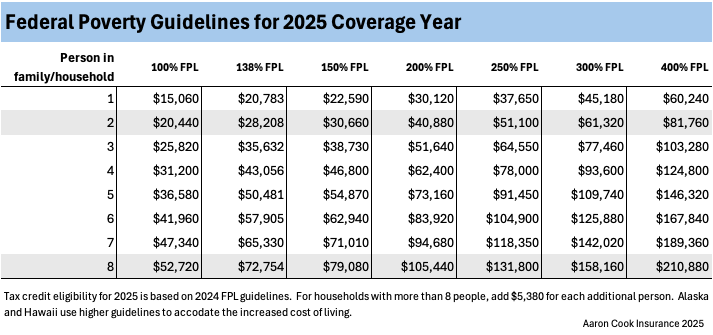

What this really means is that no one will pay more than 8.5% of their income for the Benchmark Plan. In reality, a lot of people will pay substantially less than this if their income falls below certain amounts based on the Federal Poverty Level (FPL).

The 2024 FPL guidelines are used for 2025 coverage. Income brackets as well as contribution requirements in those brackets are shown below.

How do these numbers affect my premium?

Remember the Benchmark plan we discussed above? The yearly premium cost for that plan is the number the Marketplace uses when determining what your premium should be.

Lets look at a few examples-

Assume the Benchmark Plan cost $6,000 annually. If a person earns $22,590 a year, that puts them in the 150% FPL bracket. They would not be required to pay anything for their insurance plan, so their subsidy would be $6,000.

If another person earned $37,650, or 250% of the FPL, their individual contribution would be 4%, or $1,506 per year. This person would receive an annual premium tax credit of $4,494.

The premium tax credit received can be applied to any plan sold through the Marketplace, except a Catastrophic plan. No matter the tier of the plan, the subsidy amount remains the same, so a person who decides to buy a plan that is more expensive than the Benchmark plan will be required to pay the difference. Conversely, if a person decides to buy a plan that is less expensive than the Benchmark plan, the person will have a zero-premium plan. If the subsidy is greater than the cost of the plan, the remaining credit is disregarded and lost.

Finally, there are some services and components to which the premium tax credit will not apply. PTCs can not be attributed to benefits that are not considered essential health benefits. For example, if a plan offered adult dental or vision coverage, these premiums will be added on separately after the PTC has been calculated, as routine dental and vision are not considered essential for individuals over age 19. Additionally, if you are a smoker, your PTC is not applied to the portion of the premium that is the tobacco surcharge.

How are Premium Tax Credits received?

When applying for coverage through the Marketplace, you will need to enter your household size and estimated income for the coverage year. This information generates the subsidy amount, which, once you submit the application, you will have the option to have the tax credit paid in advance, claim it when filing taxes, or a combination of the two.

If you choose to take the credit in advance, you will receive 1/12 of the tax credit paid directly to your plan’s insurer each month as an Advanced Premium Tax Credit.

Cost Sharing Reductions

Cost Sharing Reductions, or CSRs, are the second form of financial assistance available to eligible Marketplace enrollees. CSRs reduce the out-of-pocket cost that come from deductibles, copayments, and coinsurance when you use the plan.

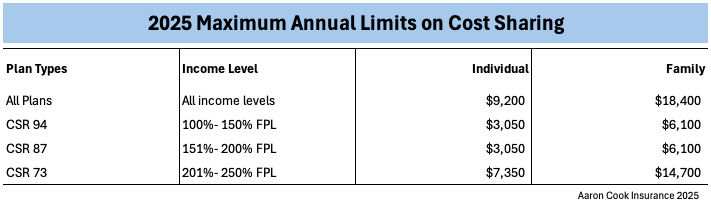

CSRs are offered to individuals and families that are both eligible for the Premium Tax Credit and whose income is between 100% and 250% of the FPL. CSRs are only available on Silver tier plans.

There are three levels of CSRs- CSR 94, 87, and 73. Each of these correlates to a percentage of the estimated cost that is reduced by the CSR. For example, a CSR 87 would reduce the estimated out-of-pocket cost by 87%.

In 2024, the average annual deductible for a silver plan was $5,000. For an individual with a CSR 94, the annual deductible was just $97. For people with a CSR 87, the average plan deductible was $700. A CSR 73 plan’s deductible was around $4,500.

What happens if I make more money than I originally estimated?

Everyone that receives an Advance Premium Tax Credit is required to file IRS form 8962 with their tax returns. This is the form that reconciles projected vs actual income in relationship to your Marketplace plan. The IRS will compare the APTC received to what should have been given based off your final reported adjusted gross income.

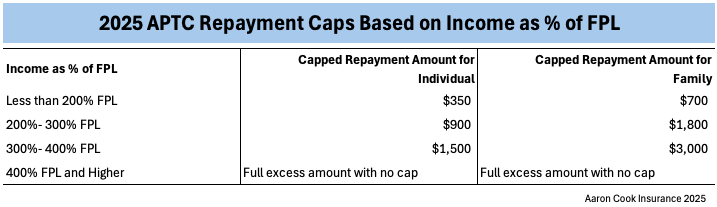

If your income is higher than you originally projected however, you will be required to repay the excess APTC, but the amount that needs to be repaid is capped based on your income.

As an example, a family at 350% FPL that owes $4,000 excess APTC would only pay $3,000.

It is highly recommended to adjust your income estimates every quarter at a minimum, or anytime that you have a life change that requires notification, such as changes to your income, address, or family size. If you fail to reconcile your APTC at the end of the year with the IRS, you will be ineligible for future APTCs.

There is no claw back for subsidies received through CSR if the estimated income is higher than what was projected.

If your income is lower than you projected, the difference is refunded to you with your tax return. In the event that overestimating caused you to miss Medicaid eligibility, you will not receive a penalty for this overestimation.

Income Verification

When you submit a plan through the Marketplace, your estimated income is almost instantly compared to your most recent tax records. To reduce fraud, if your estimated income is reduced by around 10% of the most recently reported income, you may be required to provide proof of your current income.

You will be provided a window of about 90 days to provide this information to the Marketplace, but failing to do so will result in you losing any subsidies that you may have received. If you signed up for your plan through a broker, they will be able to tell you if you need to provide income verification and help you add these documents to your account.

Takeaways

Subsidies have become synonymous with the Affordable Care Act and are one of the driving principles of Marketplace plans. Understanding how your subsidy amount is generated seems complicated, but it’s a pretty simple equation based on your income. If you still have questions or if you want to see if you qualify for a subsidy, or if you need help with income verification or changing your estimated income, feel free to reach out so that we can set up a time to talk.

- Saving on prescription medications without insurance - May 15, 2025

- What Makes One Medicare Supplement Plan Better Than Another from a Different Insurance Company? - May 12, 2025

- How your health insurance subsidy is calculated - April 28, 2025